10-Year Treasury Yield

The benchmark 10-year U.S. Treasury yield rose Monday to a level not seen in more than three years, as traders continued to assess rising inflation. The yield on the 10-year Treasury note last rose 1 basis point to 2.818%. Earlier Monday it reached its highest level since late 2018, trading above 2.87% at one point. The yield on the 30-year Treasury bond was flat at 2.91%. Yields move inversely to prices and 1 basis point is equal to 0.01%.

Bank of America- Earning Season

Bank of America profit tops estimates as lender releases reserves for soured loans. Bank of America posted first-quarter profit on Monday that exceeded analysts’ estimates, helped by the better-than-expected credit quality of its borrowers. Here are the numbers: Earnings: 80 cents a share vs 75 cents a share Refinitiv estimate. Revenue: $23.33 billion vs $23.2 billion estimate.

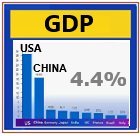

China GDP

China’s economy expanded 4.8% from a year earlier in the first three months of the year, beating market expectations as the largest domestic COVID-19 outbreaks in two years disrupted business operations and dampened consumer spending. The result, however, puts the economy on a trajectory that falls short of this year’s official target of expanding gross domestic product by 5.5%, a target that if attained would already mark the slowest annual expansion in more than a quarter-century. The outlook for the second quarter appears similarly bleak, economists say. Economists had anticipated GDP to expand by 4.6% in the first quarter, accelerating from the 4% year-on-year economic growth recorded in the final quarter of 2021.

Housing Market Index

Homebuilder sentiment drops for fourth straight month, as rising rates push housing to an inflection point. Builder confidence in the market for new single-family homes fell 2 points to 77 in April 2022, according to the National Association of Home Builders/Wells Fargo Housing Market Index. Any reading above 50 is considered positive sentiment, but the reading marks the fourth straight month of declines for the index, which stood at 83 in April 2021. Of the index’s three components, current sales conditions fell 2 points to 85. Buyer traffic dropped 6 points to 60, and sales expectations in the next six months increased 3 points to 73 following a 10-point drop in March. The housing market faces an inflection point as an unexpectedly quick rise in interest rates, rising home prices and escalating material costs have significantly decreased housing affordability conditions, particularly in the crucial entry-level market.

Housing Starts

New-home construction improves despite high inflation, rising mortgage rates, and the shortage of skilled labor and materials. U.S. homebuilding unexpectedly rose in March 2022, but starts for single-family housing tumbled amid rising mortgage rates. Housing starts increased 0.3% to a seasonally adjusted annual rate of 1.793 million units last month, the Commerce Department said on Tuesday. Data for February was revised higher to a rate of 1.788 million units from the previously reported 1.769 million units. Economists polled by Reuters had forecast starts slipping to a rate of 1.745 million units. Goldman Sachs estimates that housing starts will increase 5% to 1.7 million this year, arguing that “when housing markets are tight, like they are today, homebuilders are likely to keep building because they should have little fear that homes will sit vacant after completion.”

Building Permits

Permits for future homebuilding increased 0.4% to a rate of 1.873 million units last month, March 2022. Consequently, multifamily housing projects prevented both housing starts and building permits from declining. Permits for the construction of housing projects with five or more units rose 11% since February, and were up nearly 34% from the same time a year ago. Similarly, multifamily starts climbed 7.5% on a monthly basis and 28% from a year ago.The construction backlog continued to grow, as the number of housing projects under construction rose 2.3% from the previous month and 24% from a year ago. ..

The 30-year fixed-rate mortgage averaged 5.0% during the week ended April 14, the highest since February 2011, up from 4.72% in the prior week, according to data from mortgage finance agency Freddie Mac. Further increases are likely with the Federal Reserve adopting an aggressive monetary policy posture as it battles sky-high inflation. The Fed in March raised its policy interest rate by 25 basis points, the first hike in more than three years. Economists expect the U.S. central bank will hike rates by 50 basis points next month, and soon start trimming its asset portfolio.

IBM

IBM shares rose 3% in extended trading on Tuesday after the technology services company issued first-quarter results that beat expectations. Here’s how the company did: Earnings: $1.40 per share, adjusted, vs. $1.38 per share as expected by analysts, according to Refinitiv. Revenue: $14.2 billion, vs. $13.85 billion as expected by analysts, according to Refinitiv.

Netflix

Netflix closes down 35% wiping more than $50 billion off market cap. Netflix on Tuesday reported a loss of 200,000 subscribers during the first quarter — its first decline in paid users in more than a decade — and warned of deepening trouble ahead. Here are the key numbers from the first-quarter report: EPS: $3.53 vs, $2.89, according to a Refinitiv survey of analysts. Revenue: $7.87 billion vs. $7.93 billion, according to a Refinitiv survey of analysts. Global paid net subscriber additions: A loss of 200,000 compared with 2.73 million adds expected, according to StreetAccount estimates. Shares of Netflix closed down more than 35% Wednesday after the streamer reported earnings Tuesday evening that showed it lost subscribers for the first time in more than 10 years. The results and weak outlook led to a wave of downgrades from Wall Street on fears over the company’s long-term growth potential.

MBA Purchase Applications

Mortgage applications to purchase a home fell 3% for the week and were 14% lower than the same week one year ago. That annual decline is now beginning to grow, as housing becomes even more pricey. Mortgage demand continued to crumble last week, as mortgage rates climbed to their highest level since 2010. Total application volume fell 5% last week compared with the previous week and was nearly half of what it was one year ago, according to the Mortgage Bankers Association’s seasonally adjusted index. With rates now rising quickly after a prolonged period of hitting record lows, very few borrowers are now able to benefit from a refinance. That demand therefore fell another 8% for the week and was 68% lower than the same week one year ago. It marks six straight weeks of declines in refinancing. The refinance share of mortgage activity decreased to 35.7% of total applications from 37.1% the previous week.

Existing Home Sale

Sales of existing homes dropped 2.7% M/M in March 2022 to a seasonally adjusted, annualized rate of 5.77 million units, according to the National Association of Realtors. February’s reading was also revised downward with a larger-than-usual dent, from 6.02 million units to 5.93 million. The price of a home sold in March set a record, as inventory dwindled and sales fell. March 2022 sales were 4.5% Y/Y lower than the same period in 2021. The median price of an existing home sold in March was $375,300, an increase of 15% from March 2021. That’s the highest median price ever recorded by the Realtors. At the end of March 2022 there were 950,000 homes for sale, a decrease of 9.5% year over year. At the current sales pace that represents a two-month supply. March 2022 sales were 4.5% lower than the same period in 2021. The reading is based on closings, meaning the contracts were likely signed in January and February, when mortgage rates began to rise but had not yet shot up as sharply as they did in March. The average rate on the 30-year fixed mortgage stood at 3.29% at the beginning of January and rose to 3.9% by the end of February, according to Mortgage News Daily. The 30-year fixed rate now stands at 5.35%.

Beige Book

Beige Book: Economic activity expanded at a moderate pace. High U.S. inflation shows little sign of abating, Fed's Beige Book finds. The regular Fed survey, known as the Beige Book, found little evidence inflation is set to turn sharply lower. Businesses have been forced to pay higher wages due to a tight labor market, supply-chain bottlenecks persist and prices continued to rise. The U.S. grew steadily through early April, a Federal Reserve survey found, but high inflation showed little sign of relenting in “the coming months” and clouded the outlook for the economy.

On Wednesday, the Fed’s “Beige Book” summary of economic conditions around the U.S. noted the difficulty companies are having finding workers.Demand for workers continued to be strong across most Districts and industry sectors. But hiring was held back by the overall lack of available workers, though several Districts reported signs of modest improvement in worker availability. Many firms reported significant turnover as workers left for higher wages and more flexible job schedules. Fed officials are responding to the inflation surge with an expected series of interest rate hikes that they hope won’t derail the 2-year-old economic recovery. Markets expect the central bank’s benchmark overnight borrowing rate to rise to about 2.5% this year from near zero where it stood at the outset of 2022.

Economic activity expanded at a moderate pace since mid-February. Several Districts reported moderate employment gains despite hiring and retention challenges in the labor market. Consumer spending accelerated among retail and non-financial service firms, as COVID-19 cases tapered across the country. Manufacturing activity was solid overall across most Districts, but supply chain backlogs, labor market tightness, and elevated input costs continued to pose challenges on firms' abilities to meet demand. Vehicle sales remained largely constrained by low inventories. Commercial real estate activity accelerated modestly as office occupancy and retail activity increased. Districts' contacts reported continued strong demand for residential real estate but limited supply. Agricultural conditions were mixed across regions. Farmers were supported by surging crop prices, but drought conditions were a challenge in some Districts and increasing input costs were squeezing producer margins across the nation. Outlooks for future growth were clouded by the uncertainty created by recent geopolitical developments and rising prices.

UAL

United added roughly 12% after the airline forecasted a profit in 2022. CEO Scott Kirby told CNBC on Wednesday he’d never seen “such a hockey stick increase of demand,” referring to business travel and leisure bookings. Here’s how United performed in the first quarter compared with what Wall Street expected, based on average estimates compiled by Refinitiv: Adjusted loss per share: $4.24 versus an expected $4.22. Total revenue: $7.57 billion versus expected $7.68 billion.

Tesla - TSLA

Tesla rose about 6% after better-than-expected earnings. Those numbers were propelled in part by strong car deliveries in the quarter. Several analysts lauded Tesla after the release, with one calling it a “core holding.” Tesla just reported first-quarter earnings for 2022 and beat analysts’ expectations on the top and bottom lines. Here are the key numbers. Earnings per share: $3.22 vs $2.26 expecte. Revenue: $18.76 billion vs $17.80 billion expected Shares rose as high as 6% in after-hours trading.

Jobless Claims

Initial jobless claims last week were a bit higher than expected but still reflective of a labor market where employers are loathe to fire workers. First-time claims for benefits in the week ended April 16 totaled 184,000, a decline of 2,000 from the previous week but just ahead of the Dow Jones estimate for 182,000, the Labor Department reported Thursday. The numbers indicate the U.S. employment picture remains historically tight as job openings outnumber the available labor pool by about 5 million. Continuing claims, which run a week behind the headline number, fell by 58,000 to 1.417 million, the lowest level since Feb. 21, 1970..The jobless claims numbers reflect the continued progress in hiring. The total of those receiving benefits dropped to 1.62 million, as of data through April 2. A year ago, that total was 17.4 million, a number pared as the government has restricted extended unemployment benefits and as hiring accelerated following the release of Covid vaccines and a sharp drop in virus cases.

Philadelphia Fed Manufacturing Index

Manufacturing activity in the Philadelphia area increased less than expected in April 2022. An economic report Thursday showed that manufacturing expanded in the Philadelphia area in April 2022, but at a slower pace than expected. The Philadelphia Federal Reserve’s monthly manufacturing index registered a 17.6 reading, representing the difference between companies seeing expansion versus contraction. That was a decline of nearly 10 points from March and below the Dow Jones estimate of 21.9. Measures of new orders, shipments, unfilled orders, delivery times and the average employee workweek showed declines from March. However, prices paid and prices received both increased, reflecting continued inflation pressures, while the number of employees index also gained.

Leading Indicators

The LEI is not expected to show any effects from Russia's invasion, rising 0.3 in March 2022 percent to match February's rise. The Conference Board Leading Economic Index® (LEI) for the U.S. increased by 0.3 percent in March to 119.8 (2016 = 100), following a 0.6 percent increase in February. The LEI increased by 1.9 percent in the sixmonth period from September 2021 to March 2022. “The US LEI rose again in March despite headwinds from the war in Ukraine,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board. “This broad-based improvement signals economic growth is likely to continue through 2022 despite volatile stock prices and weakening business and consumer expectations.

Oil - Commodity

More than 17% of S&P 500 companies have reported earnings through Thursday’s open, with nearly 81% of those names beating analyst expectations, according to FactSet.

Fixed Mortage Rates

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.20% last week from 5.13%, with points rising to 0.66 from 0.63 (including the origination fee) for loans with a 20% down payment. One year ago, the rate was exactly 200 basis points lower at 3.20%. Mortgage rates continued to climb this week, as Treasury yields rose. Higher rates now appear to be hitting the nation’s homebuilders. A report Tuesday from the U.S. Census showed a drop in building permits for single-family homes. These are an indicator of future construction. Builders also reported they are now seeing much slower buyer traffic in their model homes, likely due to rising mortgage rates. Buyers hanging in the market are turning more to adjustable-rate mortgages now, which carry a lower interest rate but had been shunned as too risky following the last housing crash. The ARM share of applications reached 8.5% last week, its highest level since 2019. ARMs can be fixed rate for terms such as seven or 10 years, and are now underwritten much more carefully than they once were.

PMI Composite Flash

U.S. PMI composite flash signals composite index well below consensus. April 2022 U.S. PMI Composite Index (Flash): 55.1 vs. 57.0 consensus vs. 57.7 prior. Manufacturing Index: 59.7 vs. 58.2 consensus vs. 58.8 prior. Services Index: 54.7 vs. 58.0 consensus vs. 58.0 prior.

|