10-Year Treasury Yield

The 10-year Treasury yield inched lower Wednesday after briefly topping the 4% mark as investors bet that perhaps the Federal Reserve wouldn’t cut rates as aggressively as hoped for this year. The 10-year Treasury yield was last down more than three basis points to 3.911, after touching above the key 4% mark earlier in the morning. The 2-year Treasury yield was last trading at 4.333% after gaining half a basis point. Yields and prices have an inverted relationship and one basis point equals 0.01%.

PMI Manufacturing Final The seasonally adjusted S&P Global US Manufacturing Purchasing Managers' Index™ (PMI) posted 47.9 in December, down from 49.4 in November and lower than the earlier released 'flash' estimate of 48.2. The latest decline in the health of the sector was modest overall and the quickest since August.

Construction Spending

U.S. construction spending rose less than expected in November amid a decline in outlays on public projects, but data for the prior month was revised sharply higher suggesting underlying strength in the sector. Despite coming below expectations, the report from the Commerce Department on Tuesday added to a recent raft of data on the labor market, consumer spending and confidence in suggesting that the economy regained its poise after appearing to stumble at the start of the fourth quarter. Construction activity is being underpinned by the new single-family housing segment, thanks to an acute shortage of previously owned homes on the market. A policy by President Joe Biden's administration to bring semiconductor manufacturing back to the United States is also boosting the construction of factories, helping the keep the economy afloat. "Construction activity is one reason the Federal Reserve rate hikes have not brought the economy to its knees like the economic models from other business cycles had forecasted," said Christopher Rupkey.Construction spending shot up 11.3% on a year-on-year basis in November. Spending on private construction projects increased 0.7% in November after rising 1.2% in October.

Risk - Geopolitical

U.S. const

MBA Purchase Applications

Mortgage demand down 9.4% for final week of 2023, despite recent drop in interest rates. The average rate on the 30-year fixed ended the year at 6.76%, lower than where it was two weeks ago, but higher than it was a week ago. Applications to refinance a home loan ended the year 15% higher than the same period a year ago. Applications for a mortgage to purchase a home ended the year 12% lower.

ISM Manufacturing Index

US manufacturing sector eyes recovery in December - ISM. U.S. manufacturing contracted further in December, though the pace of decline slowed amid a modest rebound in production and improvement in factory employment. The Institute for Supply Management (ISM) said on Wednesday that its manufacturing PMI increased to 47.4 last month December 2023 after being unchanged at 46.7 for two straight months. It was the 14th consecutive month that the PMI stayed below 50, which indicates contraction in manufacturing. That is the longest such stretch since the period from August 2000 to January 2002.

The ISM Manufacturing Index Increased to 47.4 in December. Implications: The December ISM report tied a bow on what was a lousy year for the US manufacturing sector, as activity contracted for the fourteenth consecutive month, the longest streak since the aftermath of the 2000-2001 recession.

JOLTS

Job openings nudged down in November, down to lowest in more than two years. The Job Openings and Labor Turnover Survey showed employment listings nudged lower to 8.79 million, about in line with the Dow Jones estimate for 8.8 million and the lowest level since March 2021. The ratio of job openings to available workers fell to 1.4 to 1, still elevated but down sharply from the 2 to 1 level that had been prevalent in 2022. Demand for workers fell to its lowest level in more than 2½ years in November while hirings and layoffs both moved lower, the Labor Department reported Wednesday. The department’s Job Openings and Labor Turnover Survey showed employment listings nudged lower to 8.79 million, about in line with the Dow Jones estimate for 8.8 million and the lowest since March 2021. Openings fell by 62,000, though the rate of vacancies as a measure of employment was unchanged at 5.3%. Federal Reserve officials watch the JOLTS report for evidence of labor slack. The historically tight labor market had helped push inflation higher, hitting a more than 40-year peak in mid-2022 that also has slowly begun to recede.Today’s JOLTS data is another signal that the Fed is delivering a soft landing,” said Ron Temple, chief market strategist at Lazard. “Today’s report is good news for American workers and the economy, but it also suggests to me that the Fed is unlikely to cut rates as aggressively in 2024, as markets currently indicate, given the risk of reigniting inflationary pressures.

FOMC Minutes for 13/Dec/2023

Federal Reserve officials in December concluded that interest rate cuts are likely in 2024, though they appeared to provide little in the way of when that might occur, according to minutes from the meeting released Wednesday. At the meeting, the rate-setting Federal Open Market Committee agreed to hold its benchmark rate steady in a range between 5.25% and 5.5%. Members indicated they expect three quarter-percentage point cuts by the end of 2024. The minutes indicated that “clear progress” had been made against inflation, with a six-month measure of personal consumption expenditures even indicating that the inflation rate has edged below the Fed’s 2% target.

ADP Employment Report

U.S. private employers hired more workers than expected in December, pointing to persistent strength in the labor market that should continue to sustain the economy. Private payrolls increased by 164,000 jobs last month, the ADP National Employment Report showed on Thursday, the largest monthly increase since August. Data for November was revised slightly lower to show 101,000 jobs added instead of 103,000 as previously reported. Economists polled by Reuters had forecast private payrolls rising 115,000.

Jobless Claims

Jobless claims total 202,000, well below estimate.Initial claims for state unemployment benefits dropped 18,000 to a seasonally adjusted 202,000 for the week ended Dec. 30, the lowest level since mid-October. Economists polled by Reuters had forecast 216,000 claims for the latest week.

PMI Composite Final

The S&P Global US Composite PMI came in at 50.9 in December 2023, little-changed from the initial projection of 51.0 and November's 50.7. This latest figure signaled a marginal upturn in business activity, marking the swiftest expansion since July, primarily propelled by continued growth in the service sector, although manufacturing production experienced a renewed decline. Similarly, service providers saw a stronger surge in new sales, contrasting with goods producers who faced a faster decline in new business. Despite this, employment levels saw a modest increase. In terms of pricing dynamics, total input costs spiked at a sharper rate during December, while inflation in selling prices slowed down.

Nonfarm Payroll

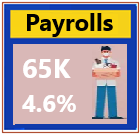

U.S. payrolls increased by 216,000 in December, much better than expected. December’s jobs report showed employers added 216,000 jobs for the month while the unemployment rate held at 3.7%. That compared with respective estimates of 170,000 and 3.8%. The hiring boost came from a gain of 52,000 in government jobs and another 38,000 in health care-related fields such as ambulatory health-care services and hospitals. Average hourly earnings rose 0.4% on the month and were up 4.1% from a year ago, both higher than the respective estimates for 0.3% and 3.9%.

Unemployment Rate

December’s jobs report showed employers added 216,000 positions for the month while the unemployment rate held at 3.7%. Economists surveyed by Dow Jones had been looking for payrolls to increase 170,000 and the unemployment rate to nudge higher to 3.8%.

ISM Service Index

Major averages meandered through the day as markets reacted to a lower than expected reading from the ISM services gauge. The measure posted a lower than expected 50.6 reading, reflecting only narrow expansion, and the lowest level of the employment component since May 2020.

Factory Orders

US factory orders rose 2.6% in November, coming higher than market estimates, and partially recovering from the steep decline in October, according to Commerce Department figures released Friday. New orders for manufactured goods increased $14.9 billion to $592.9 billion, up for the third time in the last four months. The expectation for the figure, which measures the change in the value of new purchase orders placed with manufacturers, was to show an increase of 2.1%.

Mortgage Rates

The average rate on the 30-year fixed ended the year at 6.76%, lower than where it was two weeks ago, but higher than it was a week ago.

Gold - Hedging

U.S. const

S&P 500- Index Performance Weekly

U.S. const

|