Housing Market Index - HMI

The nation’s homebuilders aren’t seeing any relief from supply chain issues that have slowed construction recently, but high buyer demand appears to be making up for it. Builder confidence in the single-family home construction market rose 4 points to 80 in October on the National Association of Home Builders/Wells Fargo Housing Market Index. That is still down from 85 in October 2020 and from the record high 90 in November of last year. Anything above 50 is considered positive.

Earning Season

Earnings could decide the fate of the mid-October market rally, as dozens of companies report in the week ahead. “We’ll have a better idea once we get through all these earnings reports coming up next week,” said one strategist. “That’s going to be the big tell. So far the initial reactions haven’t been too bad, especially given all the concerns people have had over the headwinds.The companies reporting range from Tesla and Netflix to blue chips Procter & Gamble, Johnson & Johnson, American Express, Intel and Honeywell.

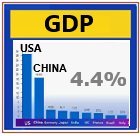

China GDP

China’s third-quarter GDP grew a disappointing 4.9% as industrial activity rose less than expected in September. The National Bureau of Statistics said Monday that gross domestic product grew 4.9% in the third quarter from a year ago. That missed expectations for a 5.2% expansion, according to analysts polled by Reuters. Industrial production rose by 3.1% in September, below the 4.5% expected by Reuters. However, retail sales beat expectations, rising 4.4% in September from a year ago. The Reuters poll predicted 3.3% growth.

Beige Book

Fed report shows wage pressures amid 'modest to moderate' economic growth.U.S. employers reported significant increases in prices and wages even as economic growth decelerated to a "modest to moderate" pace in September and early October, the Federal Reserve said on Wednesday in its latest compendium of reports about the economy. "Outlooks for near-term economic activity remained positive, overall, but some Districts noted increased uncertainty and more cautious optimism than in previous months," according to the summary of information from the Fed's 12 regional districts, prepared as part of a broad range of briefings ahead of policymakers' Nov. 2-3 meeting.

Treasury Budget

The 2021 U.S. federal fiscal year ended on a slightly better note. The federal budget deficit was $61.5 billion in September 2021, which ends the fiscal year. Fiscal year to date, the budget deficit totaled $2.77 trillion, compared with the $3.13 trillion in fiscal 2020 but noticeably higher than the approximately $1 trillion in fiscal 2019. In September 2021, federal receipts were up 23.1% on a year-ago basis to $459.5 billion. Total government spending rose by 4.7% on a year-ago basis to $521.1 billion.

Treasury International Capital (TIC)

The U.S. Department of the Treasury today released Treasury International Capital (TIC) data for August 2021. The next release, which will report on data for September 2021, is scheduled for November 16, 2021. The sum total in August of all net foreign acquisitions of long-term securities, short-term U.S. securities, and banking flows was a net TIC inflow of $91.0 billion. Of this, net foreign private inflows were $125.0 billion, and net foreign official outflows were $34.0 billion. Foreign residents increased their holdings of long-term U.S. securities in August; net purchases were $71.8 billion. Net purchases by private foreign investors were $80.2 billion, while net sales by foreign official institutions were $8.3 billion. U.S. residents decreased their holdings of long-term foreign securities, with net sales of $7.5 billion. Taking into account transactions in both foreign and U.S. securities, net foreign purchases of long-term securities were $79.3 billion. After including adjustments, such as estimates of unrecorded principal payments to foreigners on U.S. asset-backed securities, overall net foreign sales of long-term securities are estimated to have been $60.9 billion in August. Foreign residents increased their holdings of U.S. Treasury bills by $1.9 billion. Foreign resident holdings of all dollar-denominated short-term U.S. securities and other custody liabilities increased by $44.6 billion. Banks’ own net dollar-denominated liabilities to foreign residents decreased by $14.5 billion. Banks’ own net dollar-denominated liabilities to foreign residents increased by $18.1 billion.

Jobless Claims

Weekly jobless claims fall 6,000 to 290,000. Continuing claims decline 122,000 to 2.481 million. Existing home sales jump 7% in September. The number of Americans filing new claims for unemployment benefits dropped to a 19-month low last week, pointing to a tightening labor market, though a shortage of workers could keep the pace of hiring moderate in October.

Jobless claims fall again as enhanced pandemic benefits fade away. First-time filings for jobless claims totaled 290,000 for the week ended Oct. 16. That was down 6,000 from the previous week and below the 300,000 Dow Jones estimate. Continuing claims also dropped to a new pandemic low, falling to 2.48 million

Initial claims for unemployment insurance were down by 6,000 for the week ending October 16, to hit 290,000. With two consecutive weeks below 300,000, these are the lowest initial claims since March 2020. Continuing claims decreased by 122,000 for the week ending October 9, to hit 2,481,000. This is well below the 8,384,000 for the same time last year, but still above the 1.7 million pre-pandemic average. All claims, including federal programs, declined 369,992 for the week ending October 2, to hit 3,279,036. We expect UI claims to continue to normalize into yearend, signaling both ongoing progress in the labor market recovery and the end to enhanced unemployment benefits.

MBA Purchase Applications

Mortgage applications fell by 6.3 percent for the week of October 15 as both purchase and refi apps pulled back for the week. On a four-week moving average basis, purchase apps increased 2.1 percent over the month, yet were down 12 percent versus the same time last year. Refi apps were down 13.9 percent compared to a year ago. According to the Mortgage Bankers Association, the rate for a 30-year fixed rate mortgage increased to 3.23 percent. We expect rates to steadily increase as we head into 2022.

Housing Starts

Housing starts fell 1.6% in September, below expectations, the Census Bureau reported on Tuesday. Starts reached an annual rate of 1.56 million units, down from a revised 1.58 million in August. Single-family housing starts held steady in September as strong demand helped to offset ongoing supply chain disruptions. However, multifamily production declined last month, pushing overall housing starts in September down 1.6% to a seasonally adjusted annual rate of 1.56 million, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau.

The monthly housing-starts number is based on yearly sales, and calculated by assuming that September’s number is extended for a full year.

Housing starts dropped 1.6% to a seasonally adjusted annual rate of 1.555 million units last month, the lowest level since April. Data for August was revised down to a rate of 1.580 million units from the previously reported 1.615 million units.

Housing Permits

Housing starts fall 1.6% in September; August revised down. Single-family starts unchanged; multifamily drop 5.0%. Building permits tumble 7.7%; single family decrease 0.9%. U.S. homebuilding unexpectedly fell in September and permits dropped to a one-year low amid acute shortages of raw materials and labor, supporting expectations that economic growth slowed sharply in the third quarter.

PMI Composite Flash Jul. 2021

PMI composite flash signals fall in July 2021 activity. Fri, Jul. 23, 2021. July U.S. PMI Composite Flash: 59.7 vs. 63.9 prior. Manufacturing PMI: 63.1 vs. 62.1 consensus and 62.6 prior Services PMI: 59.8 vs. 64.6 consensus and 64.8 prior.

Wholesale Trade

Wholesale trade sales dropped 1.1% in August compared to July, but sales were up 20.6% from revised 2020 levels for the same period, according to the latest report from the U.S. Census Bureau. August 2021 sales of merchant wholesalers, except manufacturers’ sales branches and offices, after adjustment for seasonal variations and trading day differences but not for price changes, were $595.5 billion. Total inventories of merchant wholesalers, except manufacturers’ sales branches and offices, after adjustment for seasonal variations and trading day differences, but not for price changes, were $731.1 billion at the end of August, up 1.2% from the revised July level. Total inventories were up 12.3 percent from the revised August 2020 level. The July 2021 to August 2021 percent change was unrevised from the advance estimate of up 1.2 percent .

Existing Home Sales

Existing home sales increased in September, up 7.0 percent to hit a 6,290,000 unit annual rate. While this is the highest sales rate since January, overall existing home sales remained in the range set in the fall of 2020. The inventory of available homes on the market remained low, dipping from an already very tight 2.6 months’ worth in August, to 2.4 months in September. According to the National Association of Realtors, the median sales price of an existing home was up by 13.3 percent in September compared with a year earlier.

Philadelphia Fed Manufacturing Index Oct. 2021

The Philadelphia Fed mentioned Thursday its gauge of regional enterprise exercise fell to 23.8 in October 2021 from 30.7 within the prior month. Any studying above zero signifies bettering situations. The index had jumped sharply in September and a pullback was anticipated. Economists polled by the Wall Road Journal anticipated a 24.5 studying. Any studying above zero signifies enlargement within the manufacturing sector. A studying of 23.8 remains to be in stable development territory, economists mentioned. Manufacturing is a vivid spot within the economic system at the same time as companies wrestle to fulfill demand attributable to sudden bottlenecks. The headline index is predicated on a single stand-alone query about enterprise situations not like the nationwide ISM manufacturing index which is a composite primarily based on elements The barometer on new orders jumped 14.9 factors to 30.8. The shipments index inched up 1 level to 30. The measure on six-month enterprise outlook rose x4.2 factors to 24.2. Unfilled orders rose in October and supply occasions lengthened. Inventories slipped a bit. Costs paid rose 3 factors to 70 in October whereas the costs obtained index fell 1.8 factors. The staff index rose within the month.

Industrial Production

U.S. industrial production fell 1.3% in September 2021, much more than expected. The lingering effects of Hurricane Ida continued to stymie activity. The government said manufacturing output fell 0.7%, dragged down by a 7.2% decline in motor vehicles and parts as shortages of semiconductors continued to thwart the industry. Outside of the auto industry, factory output declined 0.3% the government said. Capacity utilization for the entire industrial sector fell 1% in September to 75.2%, about 4.4% below its average.

Leading Indicators

The Conference Board Leading Economic Index® (LEI) for the U.S. increased by 0.2 percent in September 2021 to 117.5 (2016 = 100), following a 0.8 percent increase in August and a 0.9 percent increase in July. The U.S. LEI rose again in September, though at a slower rate, suggesting the economy remains on a more moderate growth trajectory compared to the first half of the year, The Delta variant, rising inflation fears, and supply chain disruptions are all creating headwinds for the US economy. Despite the LEI’s slower growth in recent months, the strengths among the components remain widespread. Indeed, The Conference Board continues to forecast strong growth ahead: 5.7 percent year-over-year for 2021 and 3.8 percent for 2022.

|