Wholesale Trade (Pre) -Inventories

U.S. wholesale stocks rise; inventories-to-sales ratio lowest in six years. U.S. wholesale inventories increased solidly in January 2021 even as sales surged and it is taking wholesalers the shortest time in six years to clear shelves, a sign of strengthening demand that aligns with expectations for faster economic growth this year. The Commerce Department said on Monday that wholesale inventories rose 1.3% as estimated last month. Stocks at wholesalers gained 0.6% in December. The component of wholesale inventories that goes into the calculation of gross domestic product also increased 1.3% in January. Inventories rose 0.6% in January from a year earlier. Sales at wholesalers jumped 4.9% after advancing 1.9% in December. At January’s sales pace it would take wholesalers 1.24 months to clear shelves. That was the shortest since November 2014 and was down from 1.29 months in December.

Consumer Price Index (CPI) - Inflation

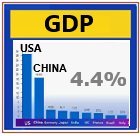

The consumer price index is expected to show a moderate gain in inflation of 0.4% in February, or 0.1% when excluding food and energy. The market is closely watching the number, as debate swirls around whether a surge in the economy – boosted by fiscal stimulus – will lead to high inflation. The Federal Reserve and many Wall Street economists expect inflation to jump but just temporarily, due to base effects of last year’s low levels of inflation when the economy was shut down. Economists expect the consumer price index rose 0.4% in February, or up 1.7% from a year ago.

That compares to a 0.3% increase in January, and a 1.4% rise on an annual basis.Economists expect the consumer price index rose 0.4% in February, or up 1.7% from a year ago. That compares to a 0.3% increase in January, and a 1.4% rise on an annual basis.Earlier on Wednesday, February’s consumer price index for February came in in-line with expectations. The Labor Department said on Wednesday its consumer price index increased 0.4% last month after rising 0.3% in January. In the 12 months through February, the CPI gained 1.7%, the largest rise since February 2020, after climbing 1.4% in January.

Concerns about higher inflation have been driving bond yields higher recently.

The $1.9 trillion fiscal stimulus package is expected to add juice to the economy. That has raised inflation concerns, and the market could be spooked by a CPI report that is any hotter than expected..

GDP

Economists estimate the economy could grow this year by as much as 7%, fueled by the massive fiscal stimulus and rollout of vaccines that are expected to get the pandemic under control. That would be the fastest growth since 1984 and would follow a 3.5% contraction last year, the worst performance in 74 years.

Treasury Budget

Last report shpw that the U.S. federal budget deficit widened in January to about five times the year-earlier level, reflecting spending on pandemic relief payments approved by Congress during the prior month.The gap increased to $162.8 billion last month, from $32.6 billion in January 2020, according to a Treasury Department report Wednesday. In the first four months of the fiscal year that began in October, the deficit amounted to $735.7 billion -- a record for the period -- compared with $389.2 billion a year earlier, before the coronavirus struck. This month the report for Feb, 2021 was $-310.9 Billions from $-162.8 Billions in January 2021.

Mortgage Applications

U.S. Treasury yields dipped slightly on Wednesday after key 10-year Treasury auction data showed enough demand to stave off fears of investors worried about a possible slump in demand for the government’s debt and a recent rapid rise in rates.The yield on the benchmark 10-year Treasury note fell about 2 basis points to 1.513% at around 3:00 p.m. ET. The yield on the 30-year Treasury bond dropped 1 basis point to 2.249%. Yields move inversely to prices (1 basis point equals 0.01%).

JOLTS

US job openings unexpectedly jumped by 165,000 in January as virus case counts hit their peak. US job openings rose to 6.9 million from 6.7 million in January, according to JOLTS data. Economists had expected a slight decline through the first month of the year. The hiring rate fell to 3.7% from 3.8% despite millions of Americans still looking for work. Job openings in the US unexpectedly climbed in January as daily new COVID-19 cases peaked and the economic recovery slowly resumed. Openings gained by 165,000 to roughly 6.9 million in the first month of the year, according to Job Openings and Labor Turnover Survey, or JOLTS, data published Thursday. Economists surveyed by Bloomberg had anticipated openings would decline slightly to 6.7 million. The state and local government education and education services sectors drove the bulk of the jump in openings, according to the report. The professional and business services industry saw the biggest drop. Roughly 1.5 Americans competed for every job in January, down from 1.6 the month prior.

Initial Jobless Claims

Weekly jobless claims rise less than expected with Biden set to sign $1.9 trillion Covid package. Jobless claims rose less than expected last week, but held above pre-pandemic levels, as President Biden prepared to sign a $1.9 trillion stimulus package. The Labor Department on Thursday reported that first-time filings for jobless benefits totaled 712,000 for the week ended March 6, below the 725,000 estimate. The Labor Department on Thursday reported that first-time filings for unemployment insurance in the week ended March 6 totaled a seasonally adjusted 712,000, below the Dow Jones estimate of 725,000. Filings for state jobless aid, seen as a proxy for layoffs, have slowed in recent weeks but remain firmly above pre-pandemic levels. The four-week moving average, which smooths out fluctuations in weekly numbers, was 759,000. The pre-Covid record for first-time applicants was 695,000.

Mortgage Rates

Mortgage rates

The average rate on the popular 30-year fixed mortgage began 2020 right around 3.75%, according to Mortgage News Daily. It then fell at the start of the pandemic in March, shot up briefly in April, when the first economic stimulus was announced, and then dropped precipitously throughout the rest of the year, setting more than a dozen record lows.

Producer Price Index PPI

U.S. producer prices moderate in February but momentum is upward. The producer price index for final demand rose 0.5% in February. U.S. producer prices increased strongly in February, leading to the largest annual gain in nearly 2-1/2 years, but considerable slack in the labor market could make it harder for businesses to pass on the higher costs to consumers.That was supported by a survey on Friday showing an easing in consumers’ near-term inflation expectations early this month, even as their confidence in the economy rose to a one-year high.

Receding new COVID-19 cases, an acceleration in the pace of vaccinations and more pandemic relief money from the government are seen allowing wider economic re-engagement in the spring. Inflation is expected to accelerate in the coming months and exceed the Federal Reserve’s 2% target, a flexible average, by April. Part of the anticipated spike would be the result of price declines early in the pandemic washing out of the calculations. Many economists, including Fed Chair Jerome Powell, do not expect the strength in inflation will persist beyond the so-called base effects.

Consumer Sentiment UM

U.S. Consumer Sentiment Advances to One-Year High on. U.S. consumer sentiment improved in early March 2021 by more than forecast . U.S. consumer sentiment improved in early March by more than forecast, reaching a one-year high as more vaccinations and fiscal relief boosted optimism in the economic outlook. The University of Michigan’s preliminary sentiment index jumped to 83.0 from 76.8 in February 2021, data released Friday showed. The figure exceeded the median projection of 78.5 in Bloomberg’s survey of economists.

Wholesale Trade

Wholesale trade improved in January compared to the same month a year ago and with December, according to the latest report from the U.S. Census Bureau. January 2021 sales of merchant wholesalers, except manufacturers’ sales branches and offices, after adjustment for seasonal variations and trading day differences but not for price changes, were $531.7 billion, up 5.9% from the revised January 2020 level and up 4.9% from the revised December 2020 level. The November 2020 to December 2020 percent change was revised from the preliminary estimate of up 1.2% to up 1.9%. Total inventories of merchant wholesalers, except manufacturers’ sales branches and offices, after adjustment for seasonal variations but not for price changes, were $661.7 billion at the end of January, up 1.3% from the revised December level. Total inventories were up 0.6% from the revised January 2020 level. The December 2020 to January 2021 percent change was unrevised from the advance estimate of up 1.3%. The January inventories/sales ratio for merchant wholesalers, except manufacturers’ sales branches and offices, based on seasonally adjusted data, was 1.24. The January 2020 ratio was 1.31. Text

|