ISM Manufacturing Index

The April Manufacturing PMI® registered 60.7 percent, a decrease of 4 percentage points from the March reading of 64.7 percent. This figure indicates expansion in the overall economy for the 11th month in a row after contraction in April 2020. April ISM manufacturing index misses expectations at 60.7

The ISM Manufacturing Index eased in April, slipping to 60.7 from 64.7 in March. The decline was a moderate surprise, as the consensus forecast had called for a slight uptick to 65.0. Despite the decline, the manufacturing economy remains on a solidly expansionary path, indicative of the broad resurgence in the economy that began last summer and continued to gather momentum in recent months.

Construction Spending

U.S. construction spending rebounded far less than expected in March as strength in housing was offset by continued weakness in outlays on nonresidential structures and public projectsThe Commerce Department said on Monday that construction spending gained 0.2% after falling 0.6% in February. Economists polled by Reuters had forecast construction spending surging 1.9%. Construction spending, which accounts for about 4% of gross domestic product, increased 5.3% on a year-on-year basis in March.

ADP Employment Report

Private payrolls grew by 742,000 in April, according to a report Wednesday from ADP. April’s total was well above the prior month’s 565,000 new jobs, but it fell short of the 800,000 Dow Jones estimate. Leisure and hospitality led gains, while manufacturing and construction also had a strong month. Private job growth accelerated in April but fell a bit short of Wall Street expectations, according to a report Wednesday from payroll processing firm ADP. Companies added 742,000 workers for the month, a jump from March’s upwardly revised 565,000 but a bit shy of the 800,000 forecast from economists surveyed by Dow Jones.

Jobless Claims

Jobless claims tumble below 500,000 in another sign the labor market is getting closer to pre-pandemic levels Initial claims for unemployment benefits fell sharply last week, sinking below 500,000 for the first time since the Covid crash. The total of 498,000 was a drop of nearly 100,000 from the previous week and below the 527,000 Dow Jones estimate. Productivity increased more than expected in the first quarter, while unit labor costs did not drop by as much as anticipated.

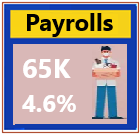

Employment Situation

Hiring was a huge letdown in April, with nonfarm payrolls increasing by a much less than expected 266,000 and the unemployment rate rose to 6.1% amid an escalating shortage of available workers. Dow Jones estimates had been for 1 million new jobs and an unemployment rate of 5.8%. Many economists had been expecting an even higher jobs number amid signs that the U.S. economy was roaring back to life. There was more bad news: March’s originally estimated total of 916,000 was revised down to 770,000, though February saw an upward revision to 536,000 from 468,000.

Trade Balance in Goods and Services

U.S. International Trade in Goods and Services, March 2021. The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $74.4 billion in March, up $3.9 billion from $70.5 billion in February, revised.

Factory Orders

New orders for U.S.-made goods rebounded in March and business spending on equipment was stronger than initially estimated, boosted by robust domestic demand, though momentum could slow because of bottlenecks in the supply chain. The Commerce Department said on Tuesday that factory orders increased 1.1% in March after falling 0.5% in February. Economists polled by Reuters had forecast factory orders rebounding 1.3%. Orders rose 6.6% on a year-on-year basis..

PMI Manufacturing Final

US manufacturing PMI up to 60.5 in April. Manufacturing activity in the United States rose significantly in April when compared to the previous month, a report published by IHS Markit on Monday showed. The seasonally adjusted Manufacturing Purchasing Managers' Index (PMI) was at 60.5 up 1.4 index points from the previous months' 59.1, marking the steepest improvement since data collection began. The rate of expansion for new orders was at an 11-year high, while job creation quickened as the backlog of work accumulated markedly. However, there was a monthly decrease in vendor performance across the goods-producing sector. Chris Williamson, Chief Business Economist at IHS Markit, commented on the report saying: "Attempts to expand capacity via hiring extra staff gained further momentum, though in some cases staff shortages were an additional constraint on production. However, with confidence in the outlook continuing to run at one of the highest levels seen over the past seven years, buoyed by vaccine roll-outs and stimulus, further investment in production capacity should be seen in coming months, helping alleviate some of the price pressures.".

PMI Composite Final Apr. 2021

U.S. PMI composite reports strongest surge in a decade amid vaccine roll-out. Wed, May 05, 2021.

April U.S. PMI Composite Index (final): 63.5 vs. 62.2 consensus and 59.7 prior. Service Index: 64.7 vs. 63.1 consensus, 60.4 prior. The Composite PMI Index posted 63.5 in April signals the sharpest upturn in private sector output since data collection began in October 2009. “Thanks to the cocktail of a successful vaccine roll-out, the reopening of the economy, ultra-accommodative monetary policy and injection of fresh fiscal stimulus, businesses are reporting the strongest surge in demand seen for at least a decade," said Chris Williamson, Chief Business Economist.

ISM Service - Non Manufacturing Index

Business Activity Index at 62.7%; New Orders Index at 63.2%; Employment Index at 58.8%; Supplier Deliveries Index at 66.1%. The Services PMI® registered 62.7 percent, which is 1 percentage point lower than last month's all-time high of 63.7 percent. The April reading indicates the 11th straight month of growth for the services sector, which has expanded for all but two of the last 135 months.The ISM Non-Manufacturing index declined to 62.7 in April, lagging the consensus expected 64.1.

Productiviy and Cost

U.S. worker productivity rebounded in the first quarter, depressing labor costs growth, but the data has been severely distorted by the COVID-19 pandemic to provide a clear trend. The Labor Department said on Thursday that nonfarm productivity, which measures hourly output per worker, increased at a 5.4% annualized rate last quarter. Data for the fourth quarter was revised higher to show productivity falling at a 3.8% rate instead of the previously reported 4.2% pace. Economists polled by Reuters had expected productivity would rebound at a 4.3% rate. Productivity shot up early in the pandemic before slumping in the final three months of 2020. Economists attributed the surge to the hollowing out of lower-wage industries, like leisure and hospitality, which they said tended to be less productive. Compared to the first quarter of 2020, productivity rose at a 4.1% pace. Hours worked increased at a 2.9% rate last quarter, slowing from a 10.0% growth pace in the October-December period. Unit labor costs - the price of labor per single unit of output - fell at a 0.3% rate. They grew at a 5.6% pace in the fourth quarter. Unit labor costs increased at a 1.6% rate from a year ago. They have also been distorted by the pandemic's disproportionate impact on lower-wage industries.

Wholesale Trade (Pre)

U.S. wholesale inventories rose sightly less than initially estimated in March 2021as sales surged amid robust demand. The Commerce Department said on Friday that wholesale inventories increased 1.3%, instead of 1.4% as estimated last month. Stocks at wholesalers gained 1.0% in February. The component of wholesale inventories that goes into the calculation of gross domestic product increased 1.3% in March. Wholesale inventories shot up 4.5% in March from a year earlier. Sales at wholesalers jumped 4.6% after being unchanged in February. Overall, business inventories were depleted in the first quarter amid a burst in domestic demand. The inventory drawdown subtracted 2.64 percentage points from GDP growth last quarter. Still, the economy grew at a robust 6.4% annualized rate in the March-January period after expanding at a 4.3% pace in the fourth quarter. At March's sales pace it would take wholesalers 1.22 months to clear shelves, down from 1.26 months in February.

Consumer Credit

U.S. consumer borrowing rose by a strong $25.8 billion in March, the second month in a row of sizable gains and a further indication that the economic recovery is picking up steam. The March gain reported Friday by the Federal Reserve followed an even larger $26.1 billion consumer-borrowing rise in February. The two monthly increases were the biggest gains since a $26.8 billion increase in December 2019, before the pandemic hit. The March borrowing advance reflected a $6.4 billion increase in the category that includes credit cards and a $19.4 billion rise in the category that covers auto loans and student loans. Consumer borrowing is watched closely for signals it can send about households' willingness to borrow to finance their spending. Consumer spending accounts for two-thirds of U.S. economic activity...

Consumer borrowing stayed strong in March after a sharp in the prior month, according to Federal Reserve data released Friday. Total consumer credit increased $25.8 billion to $4.2 trillion. That’s an annual growth rate of 7.4%, down only a fraction from the 7.5% gain in the prior month. The February gain was the largest percentage increase since December 2019. There hasn’t been two back-to-back gains in consumer credit above 7% since 2017. Economists has been expecting a $20 billion gain, according to the Wall Street Journal forecast....

|