Treasury Budget

The U.S. government's budget deficit surged to an all-time high of $1.7 trillion for the first six months of this budget year, nearly double the previous record, as another round of economic-support checks added billions of dollars to spending last month.

In its monthly budget report, the Treasury Department said Monday that the deficit for the first half of the budget year — from October through March — was up from a shortfall of $743.5 billion in the same period a year ago,

The U.S. government posted a March 2021 budget deficit of $660 billion, a record high for the month, as direct payments to Americans under President Joe Biden’s stimulus package were distributed, the Treasury Department said on Monday. The deficit for the first six months of the 2021 fiscal year ballooned to a record $1.706 trillion, compared to a $743 billion deficit for the comparable year-earlier period. The COVID-19 pandemic did not have a big impact on the first six months of fiscal 2020, as increased outlays tied to rising unemployment due to pandemic-related lockdowns and major new aid spending did not start until the very end of March 2020 and ramped up in the following month, a Treasury official told reporters.

Retail Sales

A fresh batch of stimulus checks sent consumer purchases surging in March 2021 as the U.S. economy continued to get juice from aggressive congressional spending. Retail sales rose 9.8% for the month, the Commerce Department reported Thursday. That compared to the Dow Jones estimate of a 6.1% gain and a decline of 2.7% in February.Sporting goods, clothing and food and beverage led the gains in spending and contributed to the best month for retail since the May 2020 gain of 18.3%, which came after the first round of stimulus checks.

Jobless Claims first-time filings for unemployment insurance plunged, with the Labor Department reporting 576,000 new jobless claims for the week ended April 10. That was easily the lowest total since the early days of the Covid-19 pandemic and represented a sharp decline from the previous week’s total of 769,000...mm

Empire State Manufacturing Index The New York Federal Reserve's Empire State manufacturing index fell to 24.3 in May from 26.3 in April, compared with a larger expected decrease to a reading of 23.9 in a survey compiled by Bloomberg. The Empire State index is one of the first manufacturing sector readings for May and suggests factory activity remained brisk. The new orders, shipments, and prices paid readings all increased in the month, while the employment reading declined slightly, but remained well above the breakeven point. The prices paid reading was the highest on record.

Treasury International Capital (TIC)

The U.S. Department of the Treasury today released Treasury International Capital (TIC) data for February 2021. The next release, which will report on data for March 2021, is scheduled for May 17, 2021. The sum total in February of all net foreign acquisitions of long-term securities, short-term U.S. securities, and banking flows was a net TIC inflow of $72.6 billion. Of this, net foreign private inflows were $60.9 billion, and net foreign official inflows were $11.8 billion. Foreign residents decreased their holdings of long-term U.S. securities in February; net sales were $7.3 billion. Net sales by private foreign investors were $15.3 billion, while net purchases by foreign official institutions were $7.9 billion. U.S. residents decreased their holdings of long-term foreign securities, with net sales of $11.5 billion. Taking into account transactions in both foreign and U.S. securities, net foreign purchases of long-term securities were $4.2 billion. After including adjustments, such as estimates of unrecorded principal payments to foreigners on U.S. asset-backed securities, overall net foreign sales of long-term securities are estimated to have been $38.0 billion in February. Foreign residents increased their holdings of U.S. Treasury bills by $20.7 billion. Foreign resident holdings of all dollar-denominated short-term U.S. securities and other custody liabilities increased by $13.5 billion. Banks’ own net dollar-denominated liabilities to foreign residents increased by $97.1 billion.

MBA Purchase Applications and MBS

mmmm

Business Inventories

U.S. business inventories increased solidly in February, suggesting restocking could again contribute to economic growth in the first quarter. Business inventories rose 0.5% after increasing 0.4% in January, the Commerce Department said on Thursday. Inventories are a key component of gross domestic product. February's gain was in line with economists' expectations. Inventories fell 2.4% on a year-on-year basis in February. Retail inventories were unchanged in February as estimated in an advance report published last month. That followed a ‐0.3% decline in January. Motor vehicle inventories decreased fell 2.6% as previously reported. Motor vehicle stocks are dwindling as a global semi-conductor shortage hampers auto production.,Retail inventories excluding autos, which go into the calculation of GDP, increased 1.2% as estimated last month. That followed a 0.2% gain in January.

Import and Export Prices

Import and Export Prices Surge in the Covid-19 Recovery. Import and export prices continue to surge as the recovery strengthens. U.S. import prices advanced 1.2 percent in March, 1.3 percent in February, and 1.4 percent in January. The 4.1-percent increase from December to March was the largest 3-month rise for import prices since the index advanced 5.8 percent in May 2011. The price index for U.S. imports increased 6.9 percent from March 2020 to March 2021, the largest over-the-year advance in the index since a 6.9-percent rise for the year ended January 2012.

Prices for U.S. exports increased 2.1 percent in March, after rising 1.6 percent in February and 2.6 percent in January. The 6.5-percent advance from December to March was the largest 3-month increase since the index was first published in September 1983. In March, higher prices for agricultural and nonagricultural exports both contributed to the advance in export prices. The price index for U.S. exports rose 9.1 percent from March 2020 to March 2021, the largest over-the-year increase since a 9.4-percent advance in September 2011.

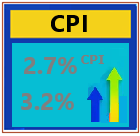

Consumer Price Index (CPI) - Inflation

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.6 percent in March on a seasonally adjusted basis after rising 0.4 percent in February, the U.S. Bureau of Labor Statistics reported today. The March 1-month increase was the largest rise since a 0.6-percent increase in August 2012. Over the last 12 months, the all items index increased 2.6 percent before seasonal adjustment.

HMI

The National Association of Home Builders/Wells Fargo Housing Market Index increased to 83, seasonally adjusted, compared to March’s reading of 82. The index tracks homebuilder confidence in current and future single-family home sales and traffic of potential homebuyers on a monthly basis.

Beige Book

Fed’s ‘Beige Book’ Shows Economy Strengthened Last Month But Supply Shortages Worsened. Companies are struggling to fill demand as shortages of labor and goods persist. The Federal Reserve's survey of its 12 regional banks, commonly called The Beige Book, portrays an economy struggling with robust demand but shortages of key ingredients such as labor, materials and low inventories of consumer goods. The economy displayed "moderate to robust growth" from late May to early July, the Fed concluded, with sectors reporting above-average growth that included transportation, travel, tourism, manufacturing and general services.

Philadelphia Fed Manufacturing Index

Philly Fed Manufacturing Index rose sharply in April 2021. US Dollar Index inches higher toward 91.70 after the data. The Federal Reserve Bank of Philadelphia reported on Thursday that the headline Manufacturing Activity Index of the Manufacturing Business Outlook Survey imorıoved to 50.2 in April from 44.5 in March. This reading beat the market expectation of 42 by a wide margin. Further details of the publication showed that the Prices Paid Index edged lower to 69.1 from 72.6, the Employment Index rose to 30.8 from 27.4 and the Six-month Business Conditions Index climbed to 66.6 from 59.1.

Industrial Production

Industrial production rebounded 1.4% in March 2021 after a revised 2.6% decline in the prior month. The Fed said industrial production jumped by 1.4 percent in March after plunging by a downwardly revised 2.6 percent in February. The rebound fell short of expectations, however, as economists had expected production to spike by 2.8 percent compared to the 2.2 percent slump originally reported for the previous month.

Total industrial production, which also includes mining and utility output, rose 1.4% in March after a revised 2.6% decrease a month earlier. The median estimate in a Bloomberg survey of economists called for a 3.6% monthly increase in factory production. The March reading was softer than forecast as automakers continued to deal with shortages of semiconductors. Capacity utilization for the industrial sector increased 1.0 percentage point in March to 74.4%, a rate that is 5.2 percentage points below its long-run (1972–2020) average.

The broader snapback in production follows on the heels of severe winter storms in February, which disrupted production and temporarily closed some plants. Output will probably remain firm in coming months against a backdrop of improving business confidence, trillions of dollars in government aid and a broader reopening economy.

JP Morgan

JPMorgan Chase beats profit estimates on strong trading, $5.2 billion release of loan-loss reserves. The bank posted first-quarter profit of $4.50 a share including a $1.28 per share benefit from the reserve release, higher than the $3.10 per share expected by analysts surveyed by Refinitiv.

Revenue of $33.12 billion exceeded the $30.52 billion estimate, driven by the firm’s trading operations, which produced about $1.8 billion more revenue than analysts had expected.

Building Permits

Applications to build, a proxy for future construction, increased 2.7% to an annualized 1.77 million units, while the number of one-family homes authorized for construction but not yet started -- a measure of backlogs -- rose to 124,000 in March, the most since May 2007. A report on Thursday showed a measure of homebuilder sentiment improved in April, suggesting firms see steady growth in the housing market heading into the second quarter. March data on both existing and new home sales will be released next week.

Housing Starts

U.S. housing starts rebounded sharply in March to the highest since 2006, exceeding forecasts and indicating residential construction is getting back on track after a winter storm-related setback. Residential starts jumped 19.4% last month to a 1.74 million annualized rate, according to government data released Friday. The median estimate in a Bloomberg survey called for a 1.61 million pace. Applications to build also climbed.

Housing Market Index - HMI

April showers may bring brighter days for homebuilders. The National Association of Home Builders/Wells Fargo Housing Market Index increased to 83, seasonally adjusted, compared to March’s reading of 82. The index tracks homebuilder confidence in current and future single-family home sales and traffic of potential homebuyers on a monthly basis. Homebuilders’ outlook on both activity from prospective buyers and single-family sales ticked up this month compared to March, but sentiment around sales in six months’ time dropped two points to a reading of 81 from 83.

Consumer Sentiment UM

Consumer sentiment rose 1.9% to 86.5 in early April, according to preliminary results from the University of Michigan Survey of Consumers. This represents a 20.5% increase year over year. Consumers in early April reported surging economic growth and strong job gains due to record stimulus spending, low interest rates, and the positive impact of vaccinations. |