10-Year Treasury Yield

nnnn

PMI Composite Final The S&P Global US Composite PMI declined to 52 in July of 2023 from 53.2 in the previous month, in line with preliminary estimates, to point to the sixth consecutive month of expansion in private-sector business activity, albeit at the softest since February. Growth was mostly supported by resilient performances in the services sector (52.3 vs 54.4 in June), offsetting a third month of contraction for manufacturers (49 vs 46.3). Aggregate new orders saw the smallest uptick in four months during the period, as rising interest rates continued to press against consumer spending. Consequently, output also edged higher at a lower pace. Still, firms continued to increase staffing numbers, largely due to faster hiring in factories. In the meantime, input prices at the aggregate level remained at historically high levels, largely due to sharp hikes in wages of service-sector employees, translating to higher output charges across the board.

Productivity and Costs

US productivity surges in second quarter; labor costs growth slows. U.S. worker productivity rebounded sharply in the second quarter, helping to curb growth in labor costs and offering another boost to the improving inflation outlook. Nonfarm productivity, which measures hourly output per worker, increased at a 3.7% annualized rate last quarter, the Labor Department said on Thursday. Data for the first quarter was revised higher to show productivity declining at a 1.2% pace instead of the previously reported 2.1% rate.

Factory Orders

US factory orders jumped 2.3% in June, higher than estimates, according to Commerce Department figures released Thursday. New orders for manufactured goods increased $13.4 billion to $592 billion, rising for the sixth time in the last seven months. Expectations for the figure, which measures the change in the value of new purchase orders placed with manufacturers, was to show a gain of 2.2%. The figure for May was revised up from a rise of 0.3% to an increase of 0.4%, while it stood at $578.6 billion that month. New orders for manufactured durable goods in June increased $13.2 billion, or 4.6%, to $302.1 billion, up for four consecutive months. The figure in May posted a gain of 2%, revised up from the previous figure of an increase of 1.8%. Transportation equipment led the increase with a gain of $12.3 billion, or 12%, to reach $115.2 billion.

MBA Purchase Applications

nnnnn

Jobless Claims

Joblmmmmm

nnnnn

mmm

ISM Manufacturing Index

Economic activity in the manufacturing sector contracted in June for the eighth consecutive month following a 28-month period of growth. The June Manufacturing PMI® registered 46 percent, 0.9 percentage point lower than the 46.9 percent recorded in May. Regarding the overall economy, this figure indicates a seventh month of contraction after a 30-month period of expansion. The New Orders Index remained in contraction territory at 45.6 percent, 3 percentage points higher than the figure of 42.6 percent recorded in May. The Production Index reading of 46.7 percent is a 4.4-percentage point decrease compared to May's figure of 51.1 percent.

Employment

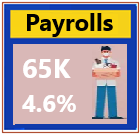

July jobs report: U.S. payroll growth totaled 187,000, lower than expected. Nonfarm payrolls expanded by 187,000 for July, slightly below the Dow Jones estimate for 200,000. The unemployment rate was 3.5%, against a consensus estimate that the jobless level would hold steady at 3.6%. Average hourly earnings rose 0.4% for the month, good for a 4.4% annual pace, both above expectations. Health care, social assistance, financial activities and wholesale trade were the leading sectors for job creation.

nnnn

U.S. lemmmmm

nnnn

nnn

Mortgage Rates

nnnnn

|