10-Year Treasury Yield

U.S. Treasury yields rose on Monday morning as concerns about inflation and economic growth remained in focus for investors. The yield on the benchmark 10-year Treasury note climbed 4 basis points to 2.832%. The yield on the 30-year Treasury bond moved 3 basis points higher to 3.031%. Yields move inversely to prices and 1 basis point is equal to 0.01%.

CFNAI - Chicago Fed National Activiy Index

Chicago Fed: "Index suggests economic growth increased in April". The Chicago Fed National Activity Index (CFNAI) increased to +0.47 in April 2022 from +0.36 in March. All four broad categories of indicators used to construct the index made positive contributions in April, and three categories improved from March. The index’s three-month moving average, CFNAI-MA3, ticked down to +0.48 in April from +0.49 in March.

PMI Composite Flash

U.S. PMI composite flash signals composite index well below consensus. May U.S. PMI Composite Index (Flash): 53.8 vs. 55.5 consensus vs. 56.0 prior. Manufacturing Index: 57.5 vs. 58.9 consensus vs. 59.7 prior. Services Index: 53.5 vs. 55.3 consensus vs. 55.6 prior.

New Home Sales

Sales of newly built homes tumbled over 16% in April 2022 while prices soared. Sales of newly built homes sank to the slowest rate since the start of the pandemic. The median price of a new home sold in April was $450,600, an increase of nearly 20% from the year before. Slower sales caused the inventory of newly built homes to jump sharply as well to a 9-month supply. A 6-month supply is generally considered balanced between buyer and seller. Sales of newly built homes dropped 16.6% in April from March, far more than expected, and were down 26.9% from April 2021, according to the U.S. Census. The annualized rate came in at 591,000 units, seasonally adjusted. Analysts had been expecting 750,000. March’s read was also revised lower. That is the slowest sales pace since April 2020, when everything shut down at the start of the pandemic. Sales surged quickly after that, as Americans sought bigger homes with outdoor spaces for quarantining.

MBA Purchase Applications

Mortgage demand slides further, even as interest rates pull back slightly. Mortgage rates turned lower for the second straight week, but it wasn’t enough to boost demand for purchase loans or refinances. Applications to refinance a home loan dropped 2% for the week and were 75% lower than the same week one year ago. Applications for a mortgage to purchase a home were flat week to week and down 16% from a year ago. Applications to refinance a home loan dropped 2% for the week and were 75% lower than the same week one year ago. Most refinance borrowers continue to remain on the sidelines as a result, and refinance applications have fallen in nine of the past 10 weeks. Compared to January 2022, refinance activity is down 66%. Homebuyers are also pulling back. Applications for a mortgage to purchase a home were flat week to week and down 16% from a year ago.

Durable Goods Orders

U.S. Durable Goods Orders Climb 0.4% In April, Less Than Expected. A report released by the Commerce Department on Wednesday showed new orders for U.S. manufactured durable goods increased by less than expected in the month of April. The Commerce Department said durable goods orders rose by 0.4 percent in April after climbing by a downwardly revised 0.6 percent in March. Economists had expected durable goods orders to advance by 0.6 percent compared to the 1.1 percent jump that had been reported for the previous month.

Dick’s Sporting Goods

Dick’s Sporting Goods shares sink after retailer cuts outlook for the year, joining broader retail trend. Here’s how Dick’s did in its fiscal first quarter compared with what Wall Street was anticipating, using Refinitiv estimates: Earnings per share: $2.85 adjusted vs. $2.48 expected. Revenue: $2.7 billion vs. $2.59 billion expected. Dick’s Sporting Goods reported results that topped Wall Street’s expectations. But the company isn’t immune to sky-high inflation and ongoing supply chain challenges. It cut its financial forecast for the full fiscal year.

FOMC minutes

Fed minutes point to more rate hikes that go further than the market anticipates. Fed minutes released Wednesday indicated that officials are prepared to move ahead with multiple 50 basis points interest rate increases. In addition, the Federal Open Market Committee said policy may have to move past “neutral” and into “restrictive” territory. The minutes indicate that members are hopeful they can bring down inflation, but also concerned about financial stability risks. On the balance sheet issue, the plan will be to allow a capped level of proceeds to roll off each month, a number that will reach $95 billion by August, including $60 billion Treasurys and $35 billion for mortgages. The minutes further indicate that an outright sale of mortgage-backed securities is possible, with notice of that happening well in advance. Market pricing currently sees the Fed moving to a policy rate around 2.5%-2.75% by the end of the year, which would be consistent with where many central bankers view a neutral rate. Statements in the minutes, though, indicate that the committee is prepared to go beyond there.

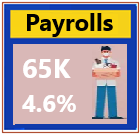

Jobless Claims

Initial jobless claims for the week ended May 21 totaled 210,000 ,a decrease from the previous 218,000, the Labor Department reported. Continuing claims, after holding around their lowest level since 1969, edged higher for the week for the week ended May 14 to nearly 1.35 million.

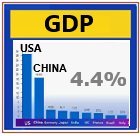

GDP

First-quarter GDP declined at a 1.5% annual pace, worse than the 1.3% Dow Jones estimate and a writedown from the initially reported 1.4%. The pullback in GDP represented the worst quarter since the pandemic-scarred Q2 of 2020. The U.S. economic contraction to start the year was worse than expected as weak business and private investment failed to offset strong consumer spending, the Commerce Department reported Thursday. First-quarter GDP declined at a 1.5% annual pace, according to the second estimate from the Bureau of Economic Analysis. That was worse than the 1.3% Dow Jones estimate and a writedown from the initially reported 1.4%. Downward revisions for both private inventory and residential investment offset an upward change in consumer spending. A swelling trade deficit also subtracted from the GDP total. The pullback in GDP represented the worst quarter since the pandemic-scarred Q2 of 2020 in which the U.S. fell into a recession spurred by a government-imposed economic shutdown to battle Covid-19. GDP plummeted 31.2% in that quarter. Economists largely expect the U.S. to rebound in the second quarter as some of the factors holding back growth early in the year subside. A surge in the omicron variant slowed activity, and the Russian attack on Ukraine aggravated supply chain issues that had contributed to a 40-year high in inflation.

Corporate Profits

US corporate profits fell in the first quarter by the most in almost two years as inflation promised greater costs for companies while the economy took a step back. Adjusted pre-tax corporate profits decreased an annualized 2.3% from the prior quarter and were up 12.5% from a year earlier, Commerce Department data showed Thursday. At the same time, one measure of profit margins edged higher. Faced with rising costs for materials, shipping and labor, many companies have sought to pass along those expenses to customers through higher selling prices. However, input costs keep rising, and consumers are grappling with decades-high inflation. In recent weeks, retailers like Target Corp. and Walmart Inc. cut their forecasts for profit this year amid bloated inventories and price increases that failed to keep up with rising costs. While companies report individual profits based on historical costs, the government adjusts the figures to reflect the current cost of replacing capital stock such as equipment and structures. Because of surging inflation, the current replacement costs are much higher.Excluding that adjustment, as well as one for inventory valuation, after-tax profits increased 1.5% in the first quarter from the end of 2021 and were up 15.7% from a year earlier.

Pending Home Sales Index

Pending home sales, a measure of signed contracts on existing homes, dropped nearly 4% in April, month to month and were down just over 9% from April 2021, according to the National Association of Realtors.The supply of homes for sale jumped 9% last week compared with the same week one year ago, according to Realtor.com.Sharply higher mortgage rates have caused a sudden pullback in home sales, and now sellers are rushing to get in before the red-hot market cools off dramatically. The supply of homes for sale jumped 9% last week compared with the same period a year ago, according to Realtor.com. That is the biggest annual gain the company has recorded since it began tracking the metric in 2017. April sales of newly built homes, also measured by signed contracts, dropped a much wider-than-expected 16% compared with March, according to the U.S. Census. Sales are slowing because mortgage rates have risen sharply since the start of the year, with the biggest gains in April and early May. The average rate on the 30-year fixed mortgage started the year close to 3% and is now well over 5%.

Fixed Mortgage Rates

Mortgage rates fell for a second consecutive week, but still remain above 5%. The 30-year, fixed-rate mortgage averaged 5.10% in the week ending May 26, down from 5.25% the week before, according to Freddie Mac. It is still well above the 2.95% average from this time last year.At the end of May 2021, a buyer who put 20% down on a $375,500 home -- a price just under the median price for an existing home -- and financed the rest with a 30-year, fixed-rate mortgage at an average interest rate of 2.95% had a monthly mortgage payment of principal and interest of $1,258, according to numbers from Freddie Mac. Today, a homeowner buying the same price house with an average rate of 5.10% would pay $1,631 a month in principal and interest. That is $373 more each month and $134,140 more in cumulative interest payments over the life of the loan, according to numbers from Freddie Mac. US home sales fell again in April as prices hit another record high.

Rates are still much higher than they were for the past two years. Last week the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 5.46% from 5.49%, with points dropping to 0.60 from 0.74 (including the origination fee) for loans with a 20% down payment.

International Trade in Goods

mmmm

Personal Income

Although inflation continued to increase in April, it was not at same magnitude as in recent months. The personal consumption expenditures (PCE) price index gained 0.2% last month after shooting up 0.9% in March. In the 12 months through April, the PCE price index advanced 6.3% after jumping 6.6% in March. The annual PCE price index increase is slowing as last year's large gains drop out of the calculation. Excluding the volatile food and energy components, the PCE price index gained 0.3%, rising by the same margin for three straight months. The so-called core PCE price index increased 4.9% year-on-year in April after rising 5.2% in March. It was the second straight month that the rate of increase in the annual core PCE price index decelerated.

Consumer Spending

U.S. consumer spending rose more than expected in April, while annual inflation appeared to have peaked, which could help to underpin economic growth in the second quarter amid rising fears of a recession. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, increased 0.9% last month, the Commerce Department said Friday. Data for March was revised higher to show outlays racing 1.4% instead of 1.1% as previously reported. Economists polled by Reuters had forecast consumer spending gaining 0.7%. Spending is being supported by strong wage gains, with companies scrambling to fill a record 11.5 million job openings as of the end of March.

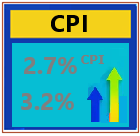

Core PCE

The Federal Reserve’s preferred inflation gauge rose 4.9% in April from a year ago, a still-elevated level that nonetheless indicated that pressures could be easing a bit. That increase in the core personal consumption expenditures price index was in line with expectations and reflected a slowing pace from the 5.2% reported in March. The number excludes volatile food and energy prices that have been a major contributor to inflation running around a 40-year peak.

The Fed's favorite inflation measure fell in April, but prices are still uncomfortably high. Another key tracker of consumer prices took a breather in April, the Commerce Department reported Friday.The price index measuring Personal Consumption Expenditures rose by 6.3% year over year in April. It was a slower pace than in March. Stripping out more volatile items like food and energy, core PCE inflation, which is the Federal Reserve's preferred measure of consumer prices, rose by 4.9% over the same period, slightly less than in March

Retail Inventories

mmmm

Wholesale Trade Advance

mmmm

Consumer Sentiment UM

mmmm |